Law Enforcement Retirement Planning: What Officers Should Review Before Leaving

Leaving law enforcement is a major financial and personal transition. Pension eligibility is important, but it is only one part of a complete retirement plan. Officers should take time to review how retirement may affect their income, health coverage, insurance, taxes, family responsibilities, and long-term financial goals.

Planning before selecting a retirement date can help identify benefits that will continue, benefits that may need to be converted or transferred, and coverage that may end when employment ends. A careful review can also reduce the risk of unexpected expenses, benefit gaps, and rushed financial decisions.

Table of Contents

- Why Retirement Planning Goes Beyond the Pension

- How Police Work Can Affect Retirement Decisions

- What Happens to Health Insurance After Retirement?

- How Do COBRA and Marketplace Coverage Work?

- What Should Officers Know About Deferred Compensation?

- Does Workplace Life Insurance Continue?

- Should an Officer Begin a Second Career?

- Law Enforcement Retirement Checklist

- Frequently Asked Questions

Why Retirement Planning Goes Beyond the Pension

A pension estimate is important, but it does not show the complete retirement picture.

An officer may also need to understand:

- Health insurance premiums

- Family coverage

- Deferred compensation

- Life insurance

- Disability benefits

- Survivor elections

- Taxes

- Debt

- Monthly expenses

- Beneficiary designations

- Future employment

An officer may be eligible to retire without being fully prepared for the financial and benefits transition.

How Police Work Can Affect Retirement Decisions

Police work may involve long periods in patrol vehicles, heavy equipment, irregular schedules, traumatic incidents, high-stress decisions, and cumulative physical wear.

The Department of Justice recognizes officer mental, physical, and financial wellness as important components of broader officer safety and wellness efforts.

An officer’s retirement decision may therefore involve more than age or years of service.

Physical health, emotional well-being, career satisfaction, family needs, and opportunities outside the department may also influence the decision.

What Happens to Health Insurance After Retirement?

Employer health coverage may change or end when an officer retires.

The available options depend on the department, union agreement, retirement system, employer plan, age, household, state, and individual eligibility.

Possible options may include:

- Retiree health coverage

- COBRA continuation coverage

- A spouse’s employer plan

- Marketplace coverage

- Medicaid

- Medicare, when eligible

- Coverage through a new employer

Officers should compare more than the premium.

They should also review provider networks, prescriptions, deductibles, out-of-pocket maximums, family coverage, and expected medical needs.

Health Coverage Options to Compare

| Coverage option | What officers should confirm | Important timing question |

|---|---|---|

| Employer retiree coverage | Premiums, dependent eligibility, provider network, prescriptions and coordination with Medicare | When does coverage begin, and can it be lost by enrolling elsewhere? |

| COBRA | Full premium, administrative cost, coverage duration and eligible dependents | What is the election deadline? |

| Spouse’s employer plan | Enrollment eligibility, family premium and network | Does loss of the officer’s coverage create a special enrollment opportunity? |

| Marketplace coverage | Eligibility, household income, available plans, provider network and prescriptions | When must the application and plan selection be completed? |

| Medicare | Eligibility date, enrollment periods, retiree-plan coordination and prescription coverage | When should enrollment begin to avoid gaps or penalties? |

| New employer coverage | Waiting period, dependent coverage and network | Will coverage begin before the previous plan ends? |

Availability and eligibility vary. Officers should confirm each option directly with the employer, plan administrator, Marketplace, Medicare, or applicable insurance provider.

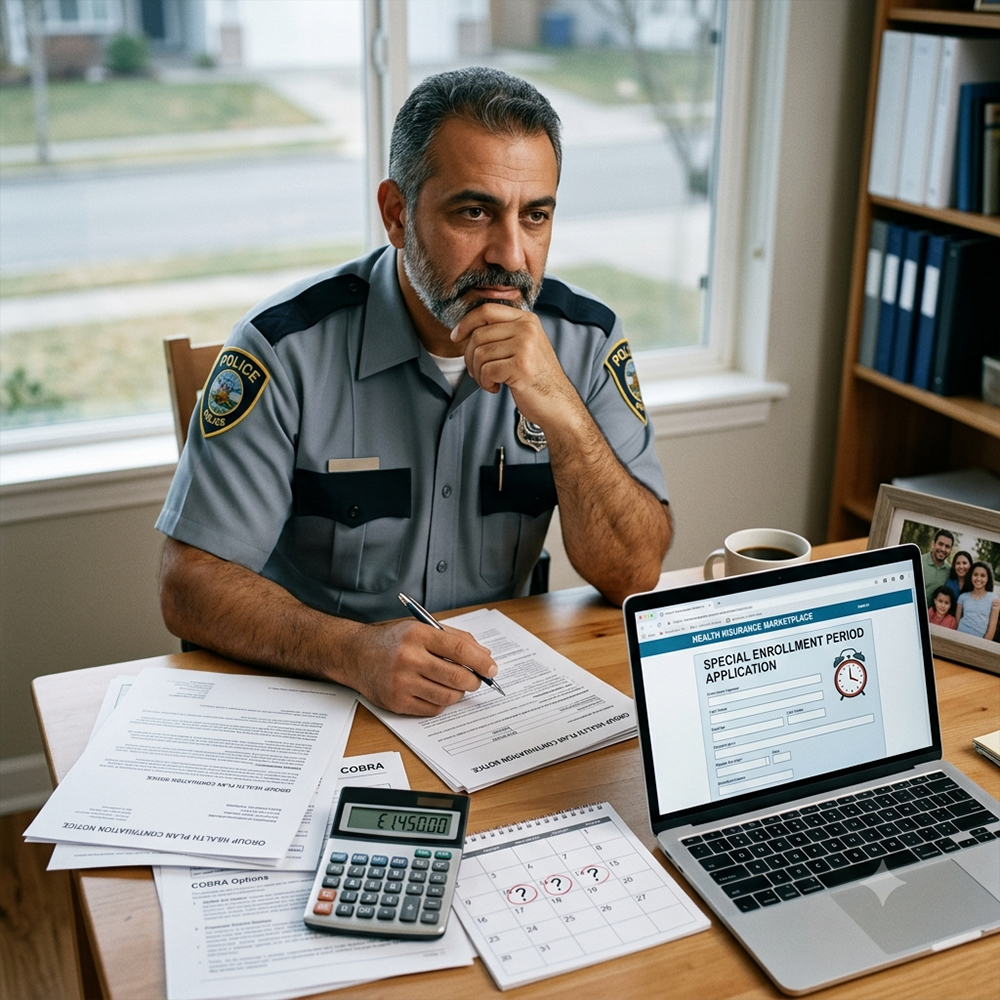

How Do COBRA and Marketplace Coverage Work?

COBRA may allow eligible employees and family members to continue the same job-based group health coverage temporarily after certain qualifying events.

The individual usually becomes responsible for the full cost of coverage, including the portion previously paid by the employer, and plans may charge an additional administrative amount.

Losing qualifying job-based coverage may also create a Marketplace Special Enrollment Period.

Eligibility must be determined through the Marketplace application, and deadlines apply.

Choosing to end COBRA voluntarily outside Open Enrollment does not always create a Special Enrollment Period. Officers should understand the timing before dropping coverage.

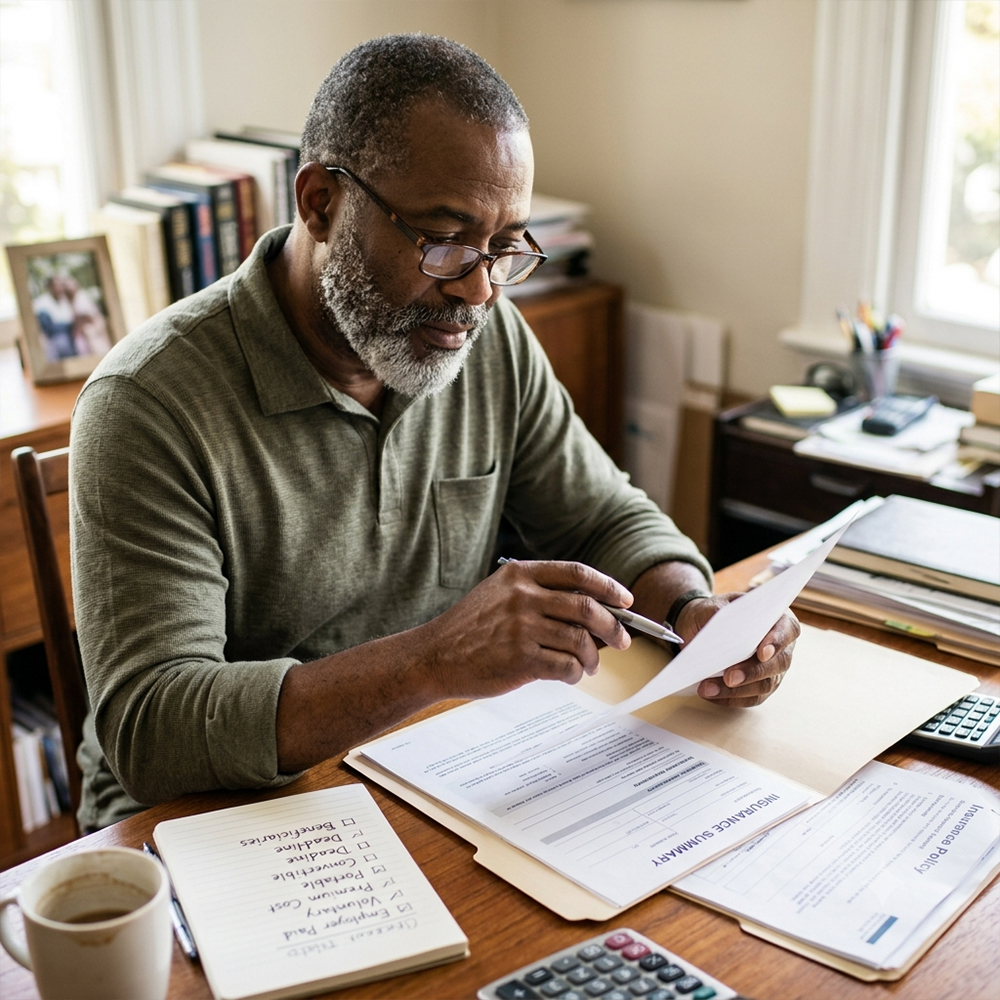

What Should Officers Know About Deferred Compensation?

Some state and local government employees may have access to a governmental 457(b) deferred compensation plan.

These plans are separate from a pension and may allow eligible employees to defer part of their compensation for retirement.

Governmental 457(b) plans have their own contribution, distribution, catch-up, and employer-specific rules.

Before retirement, officers should review:

- Current balance

- Investment allocation

- Fees

- Beneficiaries

- Employer contributions

- Distribution options

- Tax treatment

- Rollover options

- Catch-up provisions

- Withdrawal rules

Officers should consult the plan administrator and qualified tax or financial professionals before making transactions.

Does Workplace Life Insurance Continue?

Some workplace life insurance is tied directly to employment.

Other policies may be portable or convertible.

The officer should request a written benefit summary explaining:

- Which coverage is employer-paid

- Which coverage is voluntary

- Whether coverage continues

- Whether conversion is available

- Whether portability is available

- The post-employment premium

- Deadlines for making an election

- Current beneficiary information

Do not assume workplace life insurance automatically continues after retirement.

Should an Officer Begin a Second Career?

Questions Officers Should Ask Before Selecting a Retirement Date

Before selecting a final retirement date, request written answers to the following questions:

- What is my estimated monthly pension under each available survivor election?

- Have all years of service, purchased service credits, and eligible compensation been recorded correctly?

- On what exact date will my employer-sponsored health coverage end?

- Are retiree health benefits available to me, my spouse, or my dependents?

- What deadlines apply to COBRA, Marketplace coverage, Medicare, or a spouse’s employer plan?

- Can my workplace life insurance be continued, converted, or transferred after employment ends?

- What distribution, rollover, tax, beneficiary, and withdrawal options apply to my 457(b) or other deferred compensation accounts?

- Are there pension restrictions or tax consequences if I return to work?

- Which disability, union, survivor, or supplemental benefits will end when I retire?

- Which forms and elections become permanent once submitted?

Law Enforcement Retirement Checklist

Twelve to Twenty-Four Months Before Retirement

- Request a pension estimate.

- Verify service credit.

- Review survivor options.

- Gather health insurance information.

- Review deferred compensation.

- Update beneficiaries.

- List every employer and union benefit.

- Estimate retirement expenses.

- Review debt and emergency reserves.

- Consider future employment.

Six to Twelve Months Before Retirement

- Select a target retirement date.

- Compare post-employment health coverage.

- Confirm application deadlines.

- Review life insurance portability.

- Request written benefit summaries.

- Confirm tax withholding options.

- Review spouse and dependent coverage.

Before the Final Day

- Submit required pension paperwork.

- Confirm the health coverage effective date.

- Save copies of plan documents.

- Confirm beneficiary designations.

- Secure personal copies of permitted employment and benefit records.

- Confirm contact information with each plan administrator.

FAQs About Using a Health Insurance Agent

That depends on the pension amount, household expenses, debt, taxes, health insurance, family needs, savings, and future income.

No.

Depending on eligibility, other possibilities may include retiree coverage, a spouse’s employer plan, Marketplace coverage, Medicaid, Medicare, or coverage through a new employer.

Loss of qualifying job-based coverage may create a Special Enrollment Period, but eligibility and documentation requirements apply.

No.

A pension and a deferred compensation account are different benefits with different funding, distribution, investment, and tax rules.

Not always.

The plan may end, continue, convert, or allow portability, depending on the policy and employer rules.

Key Takeaways

- Law enforcement retirement planning should include more than confirming pension eligibility. Officers should review income, insurance, taxes, expenses, beneficiaries, family needs, and future employment before choosing a retirement date.

- Employer-sponsored health insurance may change or end after retirement. Possible alternatives may include retiree coverage, COBRA, a spouse’s employer plan, Marketplace coverage, Medicaid, Medicare when eligible, or coverage through a new employer.

- Health plans should be compared based on more than monthly premiums. Officers should also review provider networks, prescription coverage, deductibles, out-of-pocket limits, dependent coverage, and expected medical needs.

- Deferred compensation accounts, including governmental 457(b) plans, are separate from pension benefits. Distribution rules, taxes, fees, investments, beneficiaries, rollover options, and withdrawal requirements should be reviewed before transactions are made.

- Workplace life insurance does not always continue automatically after retirement. Officers should confirm whether coverage ends, remains active, or can be converted or transferred, along with applicable costs and deadlines.

- A second career may provide additional income, health coverage, purpose, or access to another retirement plan. Officers should consider pension restrictions, taxes, physical health, family needs, licensing requirements, and employer benefits before returning to work.

- Retirement preparation should begin well before an officer’s final day. Requesting written benefit summaries, confirming deadlines, updating beneficiaries, and comparing post-retirement coverage can reduce the risk of benefit gaps and unexpected expenses.

Next Steps

Begin by requesting an updated pension estimate and written information from every retirement plan, employer benefit program, union benefit, insurance provider, and deferred compensation administrator connected to your employment. Confirm your service credit, survivor election, beneficiaries, estimated retirement income, health-insurance termination date, life-insurance options, tax-withholding choices, and all required application deadlines.

Next, create a retirement budget that includes insurance premiums, medical expenses, taxes, debt payments, household costs, emergency reserves, and expected income from a pension, savings, deferred compensation, or future employment. Review permanent elections and financial transactions with the appropriate benefits, tax, financial, or legal professionals.

MAPFL can help law enforcement officers and their families review available post-employment health-insurance options and compare coverage based on eligibility, household needs, provider access, prescriptions, costs, and timing.

Book a free consultation to discuss potential health-insurance options before employer-sponsored coverage ends.

Call or Text MAPFL: +1-602-526-3236

Website: https://mapfl.com/

This content is provided for general educational purposes and does not constitute legal, tax, investment, financial, retirement, or insurance advice. Pension rules, retirement benefits, health coverage, deferred compensation plans, life-insurance options, tax treatment, and eligibility requirements vary by employer, retirement system, union agreement, state, household, and individual circumstances. Officers should review official plan documents and consult the appropriate benefits, tax, legal, financial, and insurance professionals before making retirement decisions.

Do not include underwriting, stop-loss, claims-fund, or employer-plan refund language in this disclaimer.

Recommended Author Display

Written by: MAPFL Editorial Team

Recommended Reviewer Display

Reviewed by: MAPFL Editorial Team (Maximize Asset Protection)

Reviewer Description

Reviewed for insurance accuracy, educational clarity, source quality, and consistency with MAPFL’s published services. Pension, tax, legal, investment, and retirement-system decisions should be verified with the appropriate qualified professionals and official plan administrators.

Get Custom Service Quote

Let's Get Connected!

Bring your health journey to life! Get a custom health plan consultation today. Let's connect and create a plan that fits your life perfectly.

Podcast Latest Episodes